Why Mortgage Rates Rose After a Fed Cut

Economy November 6, 2025

Economy November 6, 2025

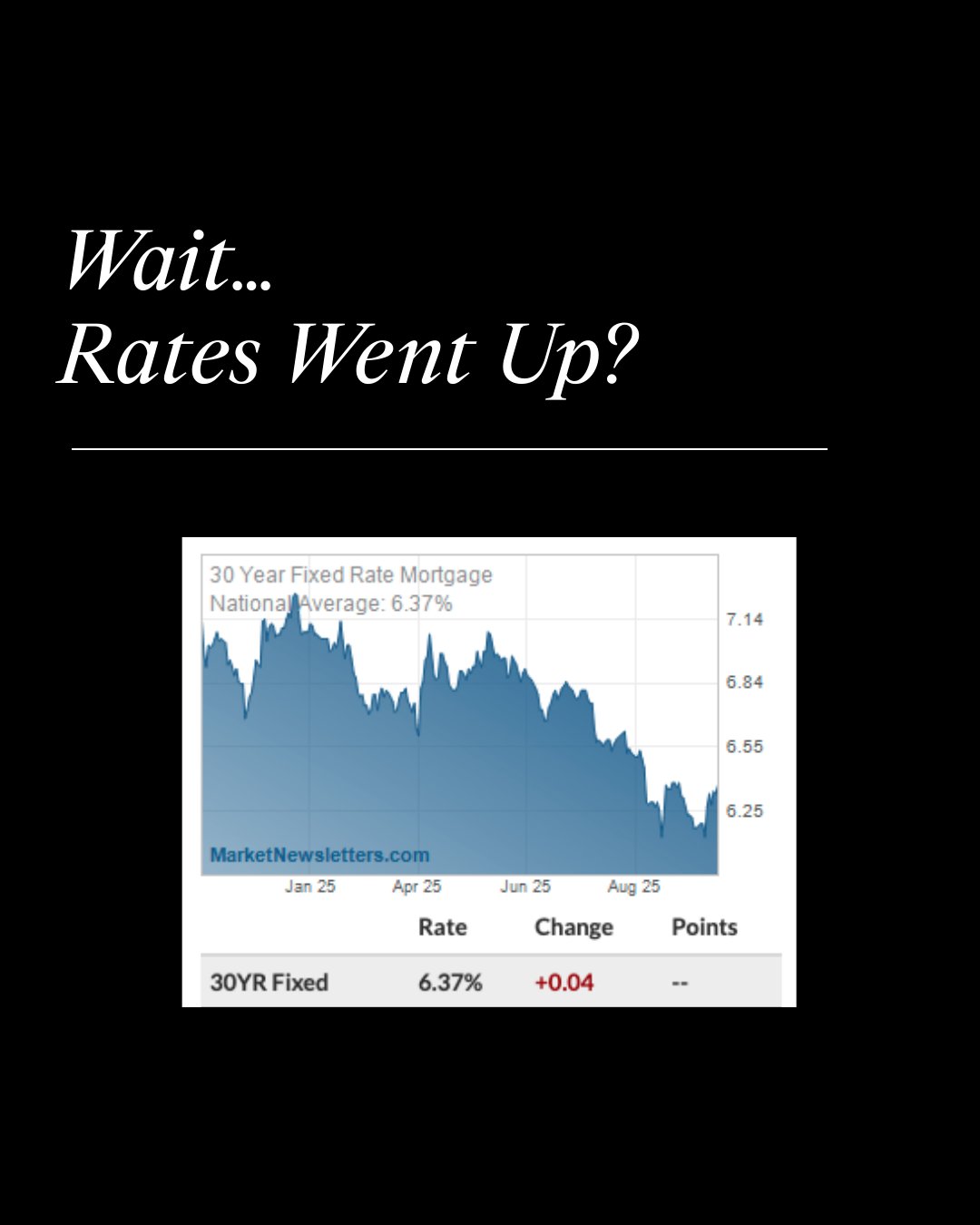

Mortgage rates are influenced by investor expectations more than by the Fed’s actions on a given day. When Chairman Powell signaled that additional cuts weren’t guaranteed, markets adjusted quickly, pushing mortgage-backed securities lower and mortgage rates higher. The takeaway: mortgage pricing reacts to perceived future policy, not to the rate announcement itself. Until economic data shows a clearer slowdown, the 30-year fixed rate may remain stuck in this mid-6% range.

Adjustable-rate mortgages (ARMs) are attracting renewed attention as buyers look for ways to manage monthly payments. ARMs currently average about a point lower than fixed loans, offering near-term savings for borrowers who expect to move or refinance within a few years. These loans differ from pre-2008 versions, with stricter underwriting and limits on rate changes, but they still carry risk if a homeowner’s plans or the broader economy shift unexpectedly.

From personal experience, I’ve used ARMs several times during seasons when our family anticipated shorter stays—typically five to seven years. In one case we stayed longer, but the rate actually adjusted down (2012 adjustment), illustrating that these products don’t always move in one direction. Still, the key is fit, not prediction: ARMs make sense only when life plans and risk tolerance align.

🔗 WSJ - Buyers Embrace Adjustable-Rate Mortgages, chancing higher payments later for lower ones now

For Greater Nashville buyers, this moment is less about reacting to rate headlines and more about maintaining perspective. Mortgage markets remain fluid, shaped by data, sentiment, and timing. Whether fixed or adjustable, the best financing choice is the one that supports your broader plan—budget, duration, and peace of mind—not a bet on where rates will go next.

Tennessee real estate tips and insights.

June 25, 2026

July 23, 2026

July 2, 2026

July 16, 2026

May 21, 2026

July 9, 2026

Bill's real estate experience spans residential and commercial transactions as an agent, buyer, seller, investor, tenant, landlord, and cross-county corporate relocation. Bill looks forward to understanding your needs, building your trust, and helping you successfully sell your existing home, find your new home, or add to your real estate portfolio.

Bill Diebenow

3990 Hillsboro Pike Suite 320 Nashville TN 37215